The Weirdest Business Expenses HMRC Has Allowed

When most people think about business expenses, they picture the usual suspects: office supplies, travel costs, maybe a laptop or a phone contract. Dull, predictable, and thoroughly uncontroversial.

But the world of allowable expenses is far stranger than you might imagine. Over the years, HMRC has accepted — and rejected — some truly bizarre claims, proving that the line between "business expense" and "nice try" is often thinner (and weirder) than anyone expected.

Before we dive in, a gentle reminder: the test for whether something qualifies as a business expense is whether it was incurred "wholly and exclusively" for the purposes of your trade. That is a strict test, but as you are about to see, it can be satisfied in some wonderfully unexpected ways.

A Bodybuilder's Baby Oil

Yes, really. Competitive bodybuilders routinely claim the cost of body oil, fake tan, and even waxing as business expenses — and HMRC has no problem with it. The reasoning is straightforward: these products are used exclusively for competition and are essential to the activity that generates income. You would not wear competition-grade body oil to Tesco on a Tuesday, so the "wholly and exclusively" test is comfortably met.

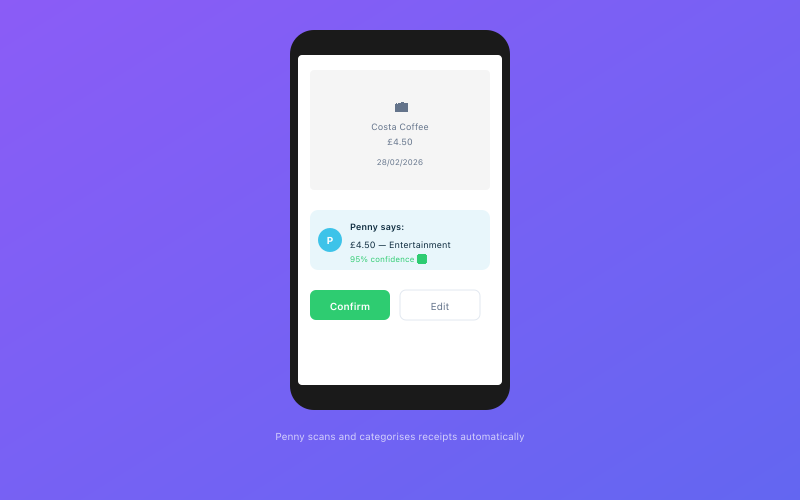

Penny scans and categorises your receipts automatically via WhatsApp

Penny scans and categorises your receipts automatically via WhatsApp

This principle extends to other performers and competitors whose work requires specific physical presentation. Actors can claim costume and make-up costs. Models can claim skincare products used exclusively for work. Dancers can claim specialised footwear and clothing.

The key word, as always, is "exclusively." If you use the same fake tan for a night out with friends, it is no longer a purely business expense. HMRC does not appreciate dual-purpose claims, no matter how bronze you look.

A Guard Dog (and Its Food)

If you run a business from premises that require security — a farm, a warehouse, a workshop — the cost of keeping a guard dog can be an allowable expense. And that includes the dog's food, veterinary bills, kennel, and other maintenance costs.

The logic is sound: the dog is performing a business function (security) that would otherwise need to be provided by some other means (an alarm system, security guard, or CCTV). The fact that the security system also happens to enjoy belly rubs and chasing squirrels is, from HMRC's perspective, irrelevant.

However — and this is important — a pet that happens to bark when someone knocks on your home office door does not qualify. The dog needs to be genuinely employed in a security capacity, and the arrangement needs to make practical business sense.

For a comprehensive look at what you can and cannot claim, our complete list of sole trader expenses is worth bookmarking.

A Cat for a Bookshop

In a delightful ruling, HMRC has accepted that a cat kept on the premises of a bookshop or similar retail establishment can be a legitimate business expense — specifically as pest control. Mice and rats can damage stock, and a cat is an environmentally friendly (and rather charming) solution to the problem.

The expense covers the cat's food, vet bills, and other maintenance costs. Whether the cat also serves as a customer attraction and Instagram content generator is beside the point — as long as its primary business function is pest management.

This principle has been extended to other businesses where animals serve a practical purpose. Farm cats, brewery cats, and warehouse cats have all found their way onto expense claims. The taxman, it turns out, is not entirely without a sense of whimsy.

Cosmetic Surgery (In Very Specific Circumstances)

Before you get excited, this is an extremely narrow exception. In a well-known case, a female actress successfully argued that breast augmentation surgery was a legitimate business expense because it was necessary to secure the roles that constituted her income. The argument was that the surgery was not for personal vanity but was a professional requirement — analogous to an athlete's knee surgery or a singer's vocal cord treatment.

HMRC accepted the claim, but this should absolutely not be taken as a green light for claiming cosmetic procedures generally. The circumstances were highly specific, and the threshold for proving that cosmetic surgery is "wholly and exclusively" for business purposes is extremely high.

The broader lesson here is that HMRC looks at the specific circumstances of each case. What matters is not what the expense is, but why it was incurred and whether the business purpose is genuine and exclusive.

A Submarine

Yes, a submarine. In a case involving a marine surveyor, the cost of a small submarine was accepted as a legitimate business expense because it was essential to conducting underwater surveys. The surveyor needed to physically inspect structures below the waterline, and a submarine was the most practical way to do so.

This is a perfect example of an expense that sounds absurd out of context but makes complete sense within it. The "wholly and exclusively" test does not care whether an expense seems unusual — it only cares whether the business genuinely needs it.

For most sole traders, a submarine is unlikely to feature on the expense claim. But the principle is instructive: if your business genuinely requires something unusual, the fact that it raises eyebrows does not automatically disqualify it.

Fancy Dress Costumes

Children's entertainers, party planners, actors, and performers can all claim the cost of costumes, fancy dress outfits, and character-specific clothing. The test is straightforward: the clothing must not be suitable for everyday wear and must be used exclusively for business purposes.

This means a clown suit, a superhero costume, or a historically accurate Tudor gown can all be claimed. A smart business suit, however, cannot — because it could equally be worn outside of work, even if you bought it specifically for client meetings.

This distinction catches many people out. The fact that you only wear a particular outfit for work does not make it a business expense. It needs to be the kind of thing you genuinely could not — or would not — wear in your personal life. A high-vis jacket for a building site? Allowable. A navy blue suit for a consulting engagement? Not allowable.

Whisky (for Research Purposes)

A whisky reviewer and writer successfully claimed the cost of purchasing whisky as a business expense, on the grounds that tasting and reviewing whisky was the core activity of their business. The whisky was not a perk of the job — it was the job.

This principle extends to food critics, wine writers, and other professionals whose work involves consuming the very product they are evaluating. The expense is allowable because the consumption is the business activity, not a personal benefit that happens to occur alongside work.

Of course, this does not mean any self-employed person can claim their Friday night wine as a business expense. The consumption must be directly and exclusively tied to income-generating activity. HMRC has a well-developed sense of the difference between research and recreation.

Expenses HMRC Has Rejected (Honourable Mentions)

Not every creative claim makes it through. Some notable rejections include:

A barrister's morning newspaper. The argument was that staying informed about current affairs was essential to legal work. HMRC disagreed, ruling that reading the newspaper was a personal activity that happened to be useful for work — not an expense incurred "wholly and exclusively" for business purposes.

A dentist's clothing. The dentist argued that they needed smart, professional clothing for work and should therefore be able to claim it. HMRC's position was clear: if you can wear it outside of work, you cannot claim it as a business expense. The fact that you choose not to is irrelevant.

A teacher's watch. The argument was that a watch was essential for timekeeping in the classroom. HMRC noted that a watch is a personal item with general utility, not a specifically professional tool. Claim rejected.

These rejections reinforce the importance of the "wholly and exclusively" test. Usefulness for work is not sufficient. The expense must have no significant personal benefit or application.

What This Means for Your Expense Claims

These unusual examples are entertaining, but they also illustrate some important principles that apply to every expense claim you make:

Context is everything. An expense that is perfectly legitimate for one business may be completely unjustifiable for another. What matters is whether the expense makes sense in the specific context of your trade.

The "wholly and exclusively" test is strict but fair. HMRC is not trying to catch you out. They are applying a clear, consistent principle. If you can genuinely demonstrate that an expense was incurred entirely for business purposes, they will accept it — even if it involves body oil or submarines.

Keep records. The more unusual the expense, the more important it is to have clear documentation of why it was incurred and how it relates to your business. A receipt alone is not enough — you need to be able to explain the business purpose if asked. Our guide on automating your receipt management can help ensure you never lose track of your documentation.

When in doubt, ask. If you are unsure whether something is allowable, consult an accountant or check HMRC's guidance before claiming it. A rejected expense is inconvenient; a penalty for a false claim is much worse.

Use good tools. Penny, Accounted's AI bookkeeping assistant, can help you categorise expenses correctly and flag anything that might need a closer look. It will not tell you whether your cat qualifies as pest control, but it will make sure your routine expenses are properly recorded and categorised.

The Bottom Line

The world of business expenses is stranger and more flexible than most people realise. HMRC is not unreasonable — they simply want to know that your claim has a genuine, exclusive business purpose. If it does, even the most unusual expense can be allowable.

That said, the vast majority of your expense claims will be perfectly ordinary: software subscriptions, phone bills, travel costs, and office supplies. Getting these right — consistently and accurately — is far more valuable than finding creative claims for body oil. The boring stuff is where the real tax savings live.

Accounted helps UK sole traders stay on top of their bookkeeping and tax. Start your free 30-day trial at getaccounted.co.uk.

Related reading:

- Sole Trader Expenses — The Complete List

- Automate Your Receipt Management

- What Your Accountant Wishes You Knew

Related Reading

Start your free trial and let Penny handle your bookkeeping automatically.

Accounted categorises your expenses automatically using AI, with confidence scores on every transaction. See how expenses work →

Tax & Compliance Specialists

Our tax specialists have decades of combined experience in UK sole trader and small business taxation, MTD compliance, and HMRC submissions. All content is reviewed against current HMRC guidance before publication and updated quarterly to reflect legislative changes.

Ready to try Accounted?

Join UK sole traders who are simplifying their bookkeeping and tax.

Start your 14-day free trial